Business Income Coverage: What Hawaiʻi Business Owners Should Know

Reading Time: 3 - 4 Minutes

Key Takeaways

- Business Income (sometimes referred to as Business Interruption) coverage helps replace lost revenue and pay continuing expenses when a covered event forces your business to temporarily close or slow down.

- Coverage is triggered by direct physical loss of or damage to your property from a covered cause of loss. Not every type of disruption qualifies.

- Two main coverage forms exist: one that includes Extra Expense coverage and one that does not. Each serves different business needs.

- Reviewing your coverage limits regularly with a licensed insurance professional helps reduce the risk of being underinsured when a loss occurs.

Disclaimer: This article is for general informational purposes only and does not constitute insurance advice, a coverage determination, or a guarantee of availability. Policy terms, conditions, exclusions, and availability vary. Please consult a licensed insurance professional for guidance specific to your business.

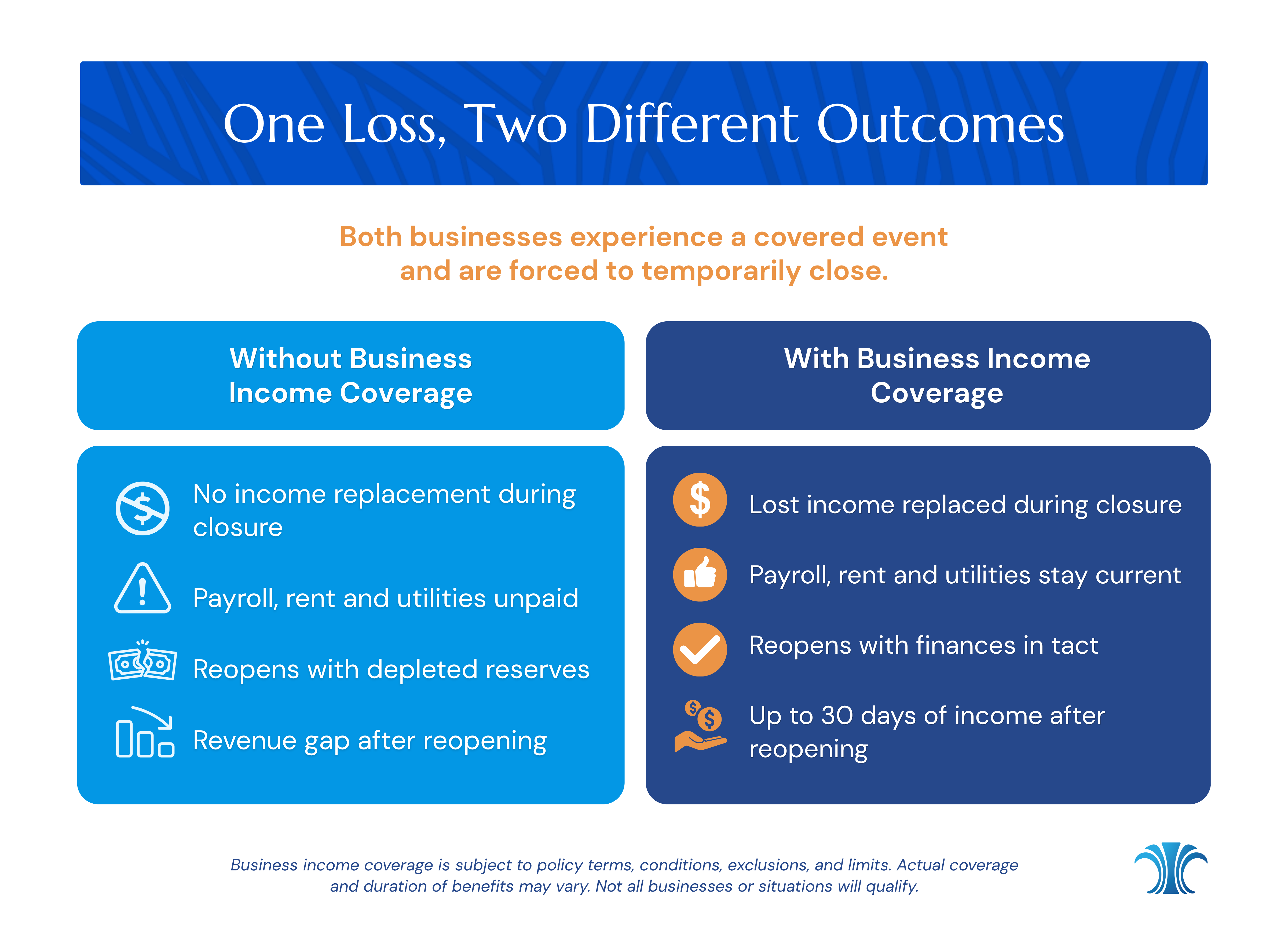

For many local business owners, property insurance feels like the obvious priority, protecting the building, the equipment, and inventory. But what happens to your business when a covered loss forces you to close, even temporarily? That's where Business Income coverage comes in, and it's a coverage business owners may overlook until it's too late.

Business Income coverage can help with operating expenses during the period of restoration, the time it takes to repair or replace damaged property and resume normal operations [1]. This article explains what it covers, how the two main coverage forms differ, and what to consider when reviewing your policy.

What Is Business Income Coverage?

Business Income (sometimes referred to as Business Interruption) coverage helps businesses protect against monetary losses due to periods of suspended operations when a covered event, such as a fire, occurs and causes direct physical loss of or damage to property [2]. In practical terms, it steps in to help replace the revenue your business would have earned if the damage had never happened.

Coverage generally includes two components: the net income your business would have earned or incurred, and the normal operating expenses that keep running even when your doors are closed, things like payroll, rent, and utilities [1].

For coverage to apply, the loss must be caused by direct physical loss of or damage to property at your described premises from a covered cause of loss. Not every type of disruption qualifies. Floods and earthquakes, for example, are generally not covered under a standard commercial property policy and typically require separate coverage [1].

What Does It Cover?

Beyond basic income replacement, Business Income policies commonly include several additional protections worth understanding.

Civil Authority Coverage applies when a civil authority (such as the governor, mayor, or police) prohibits access to your premises because of physical damage to property other than at the described premises. This coverage generally applies for up to two consecutive weeks from the date of a governmental action.

Alterations and New Buildings Coverage protects against income loss caused by damage to buildings under construction or renovation at your premises, as well as materials and equipment located nearby that are part of that work.

Extended Business Income Coverage recognizes that even after your property is repaired and you reopen, it may take time for business to return to normal. This coverage can apply for up to 30 days after the restoration period ends, or longer if your policy includes an extended period option.

Extra Expense vs. Without Extra Expense: What's the Difference?

One of the most important decisions you make regarding your Business Income coverage is whether to include Extra Expense coverage. There are two standard Business Income coverage forms: Business Income (and Extra Expense) Coverage Form and Business Income (without Extra Expense) Coverage Form.

The form with Extra Expense covers costs you incur above and beyond your normal operating expenses in order to continue or minimize the suspension of your business following a covered loss. This can include the costs associated with renting a temporary place of business while the original place of business is being restored, relocating equipment, or paying to restore lost records, expenses you would not have had if the damage had not occurred.

The form without Extra Expense is significantly narrower. It only covers expenses that directly reduce the amount of your Business Income loss, but only up to the amount of loss those expenses actually save. It does not cover the broader range of costs associated with continuing or relocating operations during repairs.

Which form makes more sense depends on your business. A company that must stay open to serve its customers such as a medical office, a grocery store, or a communications provider, may find value in the broader form. A business where operations simply cannot continue during a loss may find the narrower form sufficient. There is no one-size-fits-all answer, and the right choice depends on your specific operations, obligations, and financial situation.

Talk to Your Insurance Agent

Business Income coverage is not a simple coverage to understand, and the right structure depends on factors specific to your business: your industry, your obligations, your revenue, and your ability to continue operations after a loss. Business owners should make sure the policy limits are sufficient to cover their company for the full time it would take to rebuild and return to normal operations. After a major disaster, it can take even more time than many people realize to get back in business [1].

If you haven't reviewed your Business Income coverage recently, or if you're not sure whether your current policy includes Extra Expense coverage, reach out to your insurance agent. They can help you assess your exposure, understand your options, and make sure your coverage reflects the reality of your business today.

Frequently Asked Questions

It helps replace lost net income and covers continuing operating expenses, like payroll, rent, and utilities, while your business is closed.

No. Coverage only applies when the disruption is caused by direct physical loss or damage to property from a covered cause of loss.

One covers a broader range of costs to help you continue or relocate operations; the other only covers expenses that directly reduce your Business Income loss.

It covers income loss when a civil authority prohibits access to your premises due to physical damage to a nearby property, generally for up to two consecutive weeks.

It depends on your specific operations, obligations, and financial situation. Your insurance agent can help you decide.

Sources

1. Insurance Information Institute (III). Do I Need Business Interruption Insurance? https://www.iii.org/article/do-i-need-business-interruption-insurance

2. National Association of Insurance Commissioners (NAIC). Business Interruption Insurance/Businessowner's Policies. https://content.naic.org/cipr-topics/business-interruptionbusinessowners-policies-bop

3. International Risk Management Institute (IRMI). Business Income Coverage (BIC). https://www.irmi.com/term/insurance-definitions/business-income-coverage