Insurance Agencies and Carriers in Hawaiʻi: What's The Difference?

Reading Time: 3 – 4 Minutes

Key Takeaways

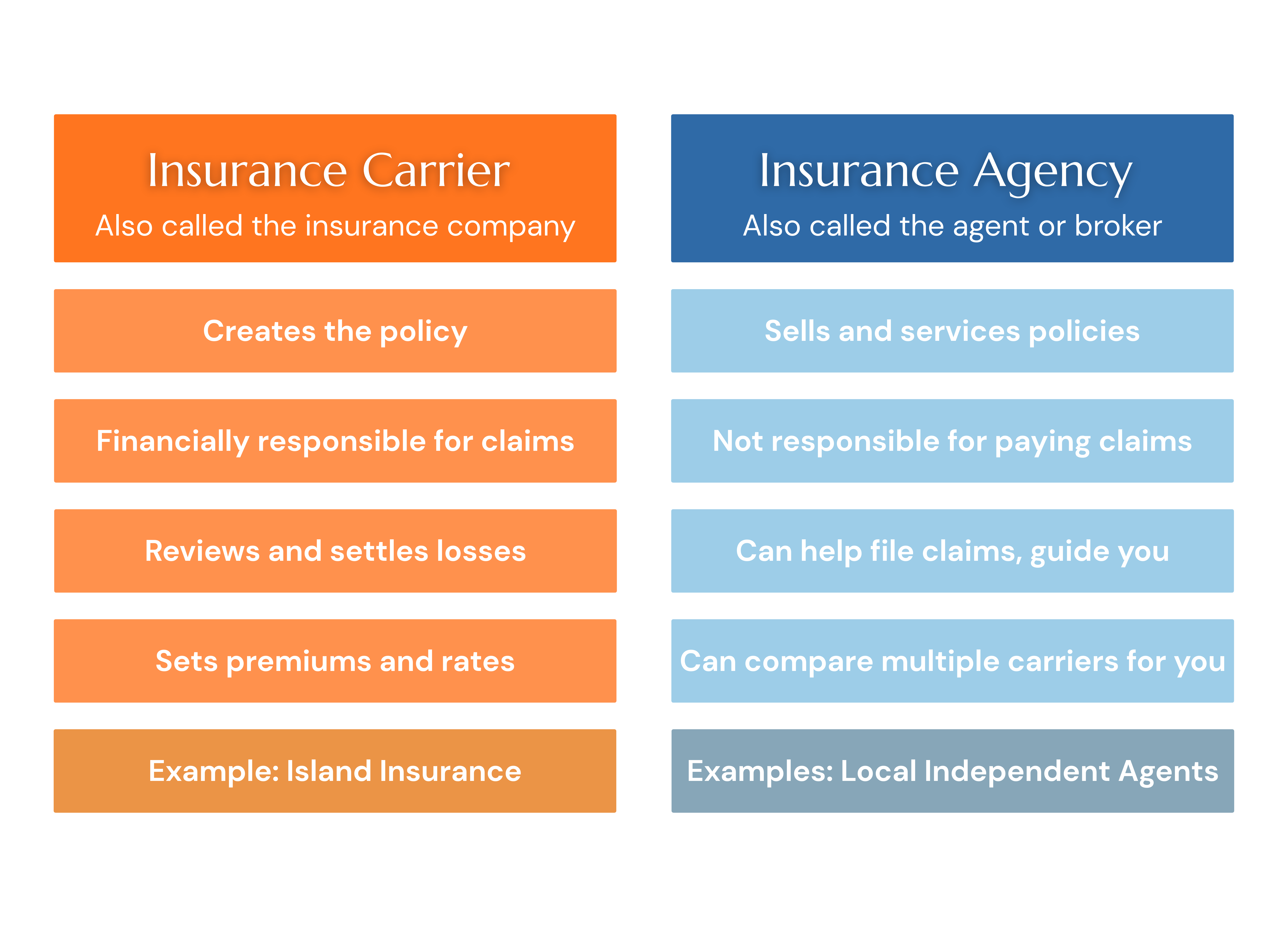

An insurance carrier creates your policy, sets its terms, and pays your covered claims. An insurance agency sells and services those policies on the carrier’s behalf.

Captive insurance agents represent one carrier. Independent insurance agents can shop multiple carriers on your behalf.

When you file a claim, the carrier reviews it and pays. The financial obligation belongs to the carrier, not the agency.

The Hawaiʻi Insurance Division licenses and oversees both carriers and agents. Residents can verify licenses and file complaints directly through the Division.

Most people don't think about insurance until something goes wrong. A fender bender on H-1, a burst pipe, a roof claim after a storm. In those moments, you're probably not thinking about policy numbers. You're thinking: is someone going to help me?

The answer often depends on two parties you may have never thought to distinguish, the insurance agency that sold you your policy and the insurance carrier that actually stands behind it. Knowing the difference can change how you shop, who you call, and what to expect when it matters most.

What Is an Insurance Carrier?

An insurance carrier, also called an insurer, is the company that creates your policy and takes on the financial risk behind it. When a covered loss occurs, the carrier is legally obligated to pay up to the limit of insurance you purchased [2]. Carriers set your premium, write your policy terms, and handle your claims.

Carriers must be licensed in every state where they operate. In Hawaiʻi, that means approval from the Hawaiʻi Insurance Division [1]. The NAIC sets national standards that help states regulate carriers consistently [2].

Island Insurance is one example. As Hawaiʻi’s only locally owned and managed property and casualty carrier, Island Insurance offers coverage for homes, condos, renters, vehicles, and businesses statewide. With over 85 years in Hawaiʻi and a financial strength rating of “A” (Excellent) from A.M. Best, we were built to support the communities and people of Hawaiʻi [3].

What Is an Insurance Agency?

An insurance agency sells policies on behalf of one or more carriers. Agents explain your options, help you select coverage, and serve as your main point of contact during the policy period. All agents in Hawaiʻi must hold a valid state license before they can sell coverage [1].

There are two types: captive agents represent a single carrier, while independent agents work with multiple carriers and can compare options on your behalf [4]. Either way, once a policy is issued, your legal agreement is with the carrier, not the agent.

A useful way to think about it: the carrier builds the product, and the agency sells it [5]. When you file a claim, the carrier takes the lead. They review it, determine coverage, and issue payment. Your agent may help you navigate the process, but the financial responsibility rests with the carrier.

The Right Person for the Right Question

Because of this distinction, carrier employees – including those at Island Insurance – are not licensed insurance agents and are not able to provide advice about your policy, recommend coverage, or guide you through coverage decisions. For any questions about what your policy covers, what changes to make, or whether your current coverage is right for your situation, your licensed insurance agent is the right person to call. They are specifically trained, licensed, and authorized to give you that guidance.

Island Insurance policies are exclusively available through independent insurance agents. Our statewide network of licensed independent agency partners can help you find the right coverage for your home, auto, or business with the added benefit of face-to-face service from people who know Hawaiʻi.

Why It Matters for Hawaiʻi Residents

That local expertise becomes especially important when you consider the risks that are unique to living and doing business in Hawaiʻi. Hawaiʻi’s exposure to hurricanes, flooding, and wildfires means that not every carrier is equally prepared for local risks. Standard home policies typically do not cover flood damage, and hurricane coverage terms vary by carrier. For auto owners, Hawaiʻi law requires a minimum level of liability coverage, and for business owners, commercial risks can include natural hazard property damage, general liability, and workers’ compensation.

Consider a homeowner in Hilo or a business owner in Honolulu. Their coverage needs are shaped by where they are, and a carrier without roots in Hawaiʻi may not be equipped to respond when it counts.

A local agent paired with a carrier that knows Hawaiʻi is a meaningful advantage.

Insurance Regulation in Hawaiʻi

Insurance in Hawaiʻi is regulated by the Hawaiʻi Insurance Division, part of the Department of Commerce and Consumer Affairs. The Division licenses carriers and agents, reviews rate and policy filings, and monitors the financial condition of insurers in the state [1]. This oversight helps ensure that the insurance market in Hawaiʻi remains stable and that licensed professionals meet consistent standards.

You can confirm that your agent and carrier are licensed at cca.hawaii.gov/ins or by calling 1-(844) 808-3222 [1].

Questions to Ask Your Agent

Are you a captive agent or independent?

Which carrier will back this policy, and are they licensed in Hawaiʻi?

Does this policy cover flood or hurricane damage, or is that separate?

Your agent is the guide. Your carrier is the entity that writes your policy. Knowing the difference tells you who to call, who pays, and whether your coverage was built for where you live.

To learn more about Island Insurance, visit islandinsurance.com or connect with a licensed agent in your area.

Disclaimer: This article is for general informational purposes only and does not constitute legal or professional insurance advice. Coverage terms, availability, and eligibility requirements vary by policy and carrier. Consult a licensed insurance professional for guidance specific to your situation.

Frequently Asked Questions

Some carriers operate as direct writers, meaning you can purchase a policy through their website or by phone without a separate agency involved. That said, working with a licensed local agent, particularly an independent one, gives you access to multiple carriers at once and someone who can help you compare options. For Hawaiʻi residents, a local agent familiar with island-specific risks can be a practical advantage when selecting coverage.

It depends on the type of insurance you are purchasing (personal or commercial), and what type of policy. When purchasing an insurance policy, talk to your agent about how to handle your claims process. Having both your agent’s contact and your carrier’s claims number saved before you need them is a smart habit.

Yes. Coverage terms, exclusions, and claims handling practices vary by carrier, and not all carriers are equally experienced with Hawaiʻi’s risk environment. Hurricane coverage, flood exclusions, and response times after major weather events can differ significantly from one company to the next. Checking a carrier’s financial strength rating through a service like A.M. Best is one way to evaluate their ability to pay claims when it matters most.

The Hawaiʻi Insurance Division offers a public license search tool where you can confirm that any agent or carrier is authorized to operate in the state. Visit cca.hawaii.gov/ins to search.

Sources

Hawaiʻi Insurance Division, Department of Commerce and Consumer Affairs. https://cca.hawaii.gov/ins/

National Association of Insurance Commissioners (NAIC). Glossary of Insurance Terms. https://content.naic.org/glossary-insurance-terms

Island Insurance. About Island Insurance. https://www.islandinsurance.com

All-Lines Training. Insurance Agent vs. Broker vs. Producer. https://alllinestraining.com/insurance-agent-broker-producer/

Insurance Information Institute (III). Background on: Buying Insurance. https://www.iii.org/article/background-on-buying-insurance

Related Articles